Friday December 17, 2010

KUALA LUMPUR: Malaysia should not go back to an agriculture-based economy

because the country would not be able to achieve the economic growth that the

Government desires and overcome unemployment, said former prime minister

Tun Dr Mahathir Mohamad.

“Sometime ago, the Government decided to focus on agriculture. However, we

have rejected agriculture because it was not able to solve the problem of

unemployment,” he said at a dialogue session on Vision 2020: Malaysia’s Looking

East concept here yesterday.

“We can still give attention to agriculture because it is making advances in terms

of technology and we cannot neglect that. But to depend entirely on agriculture

will not be productive.”

For example, he said, one acre (or 0.4ha) of land could not produce enough food

even for one family.

“However, if we build a factory on that one acre of land, then a factory can be

set up and create jobs for 500 people,” he said.

He said that even with modern agriculture, the Government would still not be able

to create enough jobs for the people.

“That is why we have switched to industrial-based economy but to do that,

we must equip our people with necessary knowledge and skills,” he said.

He said Malaysians were not inferior but instead would be able to perform like

their counterparts in Europe and Japan if they were given necessary training.

Dr Mahathir also urged the country not to rely on foreign direct investment (FDI)

for economic growth.

“Japan and South Korea did not depend on FDI but they got the technology from

other developed countries and worked with their own capacity to maximise the return

of their companies,” he said.

He said Malaysian companies now had the capacity, capital and management

to “grow big” by acquiring foreign technology.

Friday, December 17, 2010

Tuesday, December 14, 2010

PMCorp : Balance Sheet ~ 2010 Q3

First glance

Cash RM 104,096

Total Debt RM 65,062

Net Cash 6 sen per share.

Strong balance sheet.

How about "Net Cash Equavalent" assets ?

Net "Cash Equavalent" assets stands at (8+15-9) = 14 sen per share.

Net "Cash Equavalent" assets stands at (8+15-9) = 14 sen per share.If i add "unquoted invested after provision of 14 sen,

the liquidity value will be no less than (14+14) = 28 sen.

.

PMCorp current price at 12.5 sen appears "attractive" to me.

.

PMCorp : Annual Report 2009

FINANCIAL PERFORMANCE

For the financial year ended 31 December 2009, the Group recorded a revenue of RM72.9 million compared with RM125.0 million in the previous financial year. The decline in revenue was mainly due to the discontinuation of products by the Group’s food and confectionery business that did not fit with its direction or had low margins or slow sales. The rationalization of its product portfolio coupled with the rebranding of key house brands resulted in a temporary drop in revenue.

For the financial year ended 31 December 2009, the Group recorded a revenue of RM72.9 million compared with RM125.0 million in the previous financial year. The decline in revenue was mainly due to the discontinuation of products by the Group’s food and confectionery business that did not fit with its direction or had low margins or slow sales. The rationalization of its product portfolio coupled with the rebranding of key house brands resulted in a temporary drop in revenue.

.

Despite the lower revenue, the Group had achieved improved results, posting a marginal pre-tax loss of RM0.1 million compared with a pre-tax loss of RM36.2 million in the previous year. The improvement was due to significantly lower finance cost and also the stabilization of the global economy as well as strong recovery of Malaysia’s economy in the fourth quarter. The economic recovery enabled the Group to record gains on foreign exchange and a much lower allowance for diminution in value of investments compared with significant losses or allowances in the previous year. For the financial year, the Group’s results were affected by higher advertising and promotion expenditure incurred for its product rebranding exercise.

.

The Group had in December 2008 and January 2009 repaid a substantial amount of its banks borrowings. This improved the financial position of the Group, thus placing the Group in a better position to focus and channel its resources on expanding its food and confectionery business.

.

REVIEW OF OPERATIONS

.

The Group is primarily engaged in the manufacturing, marketing and distribution of food and confectionery products through its wholly-owned subsidiary company, Network Foods International Ltd (NFIL). The Network Foods group operates out of Malaysia, Singapore and Hong Kong and exports to more than 50 countries.

.

Malaysia

.

In Malaysia, the Group’s operations are undertaken by two NFIL subsidiaries, Network Foods Industries Sdn Bhd (NFI) and Network Foods (Malaysia) Sdn Bhd (NFM).

.

The Group had in December 2008 and January 2009 repaid a substantial amount of its banks borrowings. This improved the financial position of the Group, thus placing the Group in a better position to focus and channel its resources on expanding its food and confectionery business.

.

REVIEW OF OPERATIONS

.

The Group is primarily engaged in the manufacturing, marketing and distribution of food and confectionery products through its wholly-owned subsidiary company, Network Foods International Ltd (NFIL). The Network Foods group operates out of Malaysia, Singapore and Hong Kong and exports to more than 50 countries.

.

Malaysia

.

In Malaysia, the Group’s operations are undertaken by two NFIL subsidiaries, Network Foods Industries Sdn Bhd (NFI) and Network Foods (Malaysia) Sdn Bhd (NFM).

.

NFI manufactures chocolate and confectionery products under established brands such as Tudor Gold, Crispy, Tango, Kandos and Kiddies.

.

During the year under review, NFI’s revenue decreased by 30.1% to RM47.5 million due to weak market sentiments in the domestic market. However, exports continued to increase and contributed 50% of its total sales.

.

During the year, the company undertook a major rebranding exercise for several of its products. This undertaking, which involved the improvement of product quality, taste and packaging, successfully elevated their brand positioning and greatly improved market acceptance.

.

During the year, the company undertook a major rebranding exercise for several of its products. This undertaking, which involved the improvement of product quality, taste and packaging, successfully elevated their brand positioning and greatly improved market acceptance.

.

For the financial year under review, the company recorded a reduced profit of RM3.2 million. The lower profit was due to the significantly higher advertising and promotion expenditure that was necessary to relaunch the upgraded products.

.

As part of the company’s continual effort to grow its markets, NFI will strive to secure ISO22000:2005 standards so as to be able to export to Britain and European Union countries. ISO22000:2005 is a Food Safety Management System in the International Organization for Standardization and will be used in tandem with our existing ISO9001:2008 and HACCP certifications.

.

NFM is the marketing and distribution arm of the Network Foods group and also acts for other agency lines in the distribution of their products.

.

For the financial year under review, NFM recorded a lower revenue of RM32.9 million due to temporary market disruptions resulting from product rationalization undertaken by the company as well as its ongoing exercise to improve product quality, taste and packaging. Consequently, NFM suffered a loss before tax of RM4.3 million. During this transitional period, NFM continued to relaunch some existing house brands while adding new agency lines, and creating new house brands on other food items. It expects to return to profitability in this financial year.

.

NFI completed the acquisition of the piece of property adjoining its existing factory in Shah Alam. The enlarged site will allow for the Group’s manufacturing, sales and distribution divisions to be situated in one central location. This will result in improved efficiencies and better synergies in the operations of the two companies as well as making adequate allowance for future growth in manufacturing and warehousing capacity. Construction is expected to commence in the second half of 2010.

.

Singapore and Hong Kong

.

The operations of the Group in Singapore and in Hong Kong are undertaken by Network Foods Distribution Pte Ltd (NFD) and Network Foods (Hong Kong) Ltd (NFHK) respectively. During the year under review, NFD undertook aggressive marketing to establish the revamped Tudor Gold and Crispy brands. This has led to an improvement in revenue and profitability in the fourth quarter of 2009. Despite operating under a difficult economic environment in Hong Kong, NFHK performed satisfactorily in 2009 and managed to record revenue and profit which are comparable to the previous year.

.

.

Singapore and Hong Kong

.

The operations of the Group in Singapore and in Hong Kong are undertaken by Network Foods Distribution Pte Ltd (NFD) and Network Foods (Hong Kong) Ltd (NFHK) respectively. During the year under review, NFD undertook aggressive marketing to establish the revamped Tudor Gold and Crispy brands. This has led to an improvement in revenue and profitability in the fourth quarter of 2009. Despite operating under a difficult economic environment in Hong Kong, NFHK performed satisfactorily in 2009 and managed to record revenue and profit which are comparable to the previous year.

.

Collected another 40,000 PMCorp shares at 12.5 sen

Pan Malaysia Corporation

Today, I collected another 40,000 PMCorp shares at 12.5 sen.

Wish me LUCK !

.

Today, I collected another 40,000 PMCorp shares at 12.5 sen.

Wish me LUCK !

.

Monday, December 13, 2010

Perodua outlines its green strategy

Monday, December 13, 2010

"In the meantime, we will refocus on improving our internal combustion engine to be as good as those trending new green technologies," he said. Currently, the company is pushing for more improvements for its internal combustion engine by replacing its cast iron engine parts to full aluminum components in the first stage of its roadmap.

"Although we are still on internal combustion engines and with the effort that we have put in these engines will be on the same footing with hybrid and EV technologies. "The first stage is in the works, and the products would hit the market anytime in the next two to three years," he said.

Perodua is also working on a two-cylinder direct injection turbo-charged engine under its second stage roadmap for engine development. "The car will have more power by then with the extra boost and we strongly believe that with the turbo charged engines, we can improve fuel efficiency and cut down on carbon emissions, both by 30 per cent," he said.

Elaborating on the Electronic Automatic Transmission (E-AT) system meant for production soon, he said it has reached the final stage of production study. "We need to set up a completely different plant for the E-AT systems, and I'm sure investments of more than RM150 million will be made and production will start within two to three years. "We are currently going into the details like the plant layout and selecting the vendors that can help us put some of the components together," he said.

He added investments made could be considered as domestic direct investments (DDI), answering the government's call for the private sector to invest more. "This is the kind of technology transfer we desire from Daihatsu and they will help us train our local engineers, operators and vendors to be compliant. "E-AT is a high-technology dust free extremely sensitive system and quality is of the paramount criteria this time," he said.

With the move to reduce its carbon footprint and improve fuel efficiency, Aminar is calling on the government to recognise the carmaker's efforts and extend incentives for hybrid vehicles and EV to Perodua too. Besides, he added the company would continue to improve the plant's manufacturing facilities as well.

Touching on the widely discussed Proton-Perodua merger, he said the company does not know the outcome and recommendations of the study. "Let's wait for the announcement but we will proceed with our roadmap and address the issues as well as weaknesses we have currently.

"Allow us, together with Daihatsu, to continue on this exciting journey that we have. It will require some time to execute but this is the future as we see it," he said.

-Bernama

"In the meantime, we will refocus on improving our internal combustion engine to be as good as those trending new green technologies," he said. Currently, the company is pushing for more improvements for its internal combustion engine by replacing its cast iron engine parts to full aluminum components in the first stage of its roadmap.

"Although we are still on internal combustion engines and with the effort that we have put in these engines will be on the same footing with hybrid and EV technologies. "The first stage is in the works, and the products would hit the market anytime in the next two to three years," he said.

Perodua is also working on a two-cylinder direct injection turbo-charged engine under its second stage roadmap for engine development. "The car will have more power by then with the extra boost and we strongly believe that with the turbo charged engines, we can improve fuel efficiency and cut down on carbon emissions, both by 30 per cent," he said.

Elaborating on the Electronic Automatic Transmission (E-AT) system meant for production soon, he said it has reached the final stage of production study. "We need to set up a completely different plant for the E-AT systems, and I'm sure investments of more than RM150 million will be made and production will start within two to three years. "We are currently going into the details like the plant layout and selecting the vendors that can help us put some of the components together," he said.

He added investments made could be considered as domestic direct investments (DDI), answering the government's call for the private sector to invest more. "This is the kind of technology transfer we desire from Daihatsu and they will help us train our local engineers, operators and vendors to be compliant. "E-AT is a high-technology dust free extremely sensitive system and quality is of the paramount criteria this time," he said.

With the move to reduce its carbon footprint and improve fuel efficiency, Aminar is calling on the government to recognise the carmaker's efforts and extend incentives for hybrid vehicles and EV to Perodua too. Besides, he added the company would continue to improve the plant's manufacturing facilities as well.

Touching on the widely discussed Proton-Perodua merger, he said the company does not know the outcome and recommendations of the study. "Let's wait for the announcement but we will proceed with our roadmap and address the issues as well as weaknesses we have currently.

"Allow us, together with Daihatsu, to continue on this exciting journey that we have. It will require some time to execute but this is the future as we see it," he said.

-Bernama

Sunday, December 12, 2010

When Stock Prices Drop, Where's the Money?

QUOTED from BB investing notes Blogsite

When Stock Prices Drop, Where's the Money?

by Investopedia Staff

Monday, March 16, 2009

Have you ever wondered what happened to your socks when you put them into the dryer and then never saw them again? It's an unexplained mystery that may never have an answer. Many people feel the same way when they suddenly find that their brokerage account balance has taken a nosedive. So, where did that money go? Fortunately, money that is gained or lost on a stock doesn't just disappear. Read to find out what happens to it and what causes it.

Disappearing Money

Before we get to how money disappears, it is important to understand that regardless of whether the market is in bull (appreciating) or bear (depreciating) mode, supply and demand drive the price of stocks, and fluctuations in stock prices determine whether you make money or lose it.

So, if you purchase a stock for $10 and then sell it for only $5, you will (obviously) lose $5. It may feel like that money must go to someone else, but that isn't exactly true. It doesn't go to the person who buys the stock from you. The company that issued the stock doesn't get it either. The brokerage is also left empty-handed, as you only paid it to make the transaction on your behalf. So the question remains: where did the money go?

Leno's Response ~

This is an example of simple things are perceived wrongly or at least i will csaid "mal-represented." The answer or explanation lies firstly by re-correcting the "mal-representation," or simply re-stated the whole perception from the beginning.

When I bought a "second-hand" car from someone (similar as stocks which are traded thru secondary market), I will pay a certain amount for eg. RM 20,000 to Abu. Now, i am less RM 20,000 in my bank or just let presume my bank balance left zero after witdrew to pay Abu, in exchange for the ownership of the "CAR."

If another car of the same type is transacted at RM 15,000, let's say in between Ah Chong and Ramasamy, could we safely presumed my car has depreciated by RM 5,000 ?

If another car of the same type is transacted at RM 25,000 again between others buyer and seller, could I say, "WHOA ! I just made RM 5,000 !" ?

Funny right ? Of course by now, someone will try to educate me about the so-call "paper" loss or gain.

Now, let's say I sell-off my Car at RM 15,000 to Jay. Therefore Jay will have "less RM 15,000" by owning the car, Abu (the one who sold the car to me at the first place) still holding RM 20,000 but with no car and, I will have RM 15,000 and car-less as well.

When Stock Prices Drop, Where's the Money?

by Investopedia Staff

Monday, March 16, 2009

Have you ever wondered what happened to your socks when you put them into the dryer and then never saw them again? It's an unexplained mystery that may never have an answer. Many people feel the same way when they suddenly find that their brokerage account balance has taken a nosedive. So, where did that money go? Fortunately, money that is gained or lost on a stock doesn't just disappear. Read to find out what happens to it and what causes it.

Disappearing Money

Before we get to how money disappears, it is important to understand that regardless of whether the market is in bull (appreciating) or bear (depreciating) mode, supply and demand drive the price of stocks, and fluctuations in stock prices determine whether you make money or lose it.

So, if you purchase a stock for $10 and then sell it for only $5, you will (obviously) lose $5. It may feel like that money must go to someone else, but that isn't exactly true. It doesn't go to the person who buys the stock from you. The company that issued the stock doesn't get it either. The brokerage is also left empty-handed, as you only paid it to make the transaction on your behalf. So the question remains: where did the money go?

Leno's Response ~

This is an example of simple things are perceived wrongly or at least i will csaid "mal-represented." The answer or explanation lies firstly by re-correcting the "mal-representation," or simply re-stated the whole perception from the beginning.

When I bought a "second-hand" car from someone (similar as stocks which are traded thru secondary market), I will pay a certain amount for eg. RM 20,000 to Abu. Now, i am less RM 20,000 in my bank or just let presume my bank balance left zero after witdrew to pay Abu, in exchange for the ownership of the "CAR."

If another car of the same type is transacted at RM 15,000, let's say in between Ah Chong and Ramasamy, could we safely presumed my car has depreciated by RM 5,000 ?

If another car of the same type is transacted at RM 25,000 again between others buyer and seller, could I say, "WHOA ! I just made RM 5,000 !" ?

Funny right ? Of course by now, someone will try to educate me about the so-call "paper" loss or gain.

Now, let's say I sell-off my Car at RM 15,000 to Jay. Therefore Jay will have "less RM 15,000" by owning the car, Abu (the one who sold the car to me at the first place) still holding RM 20,000 but with no car and, I will have RM 15,000 and car-less as well.

Let's rephrase whole scenario using a table

Previously,

Abu got 1 car / RM 0 cash

I.. got 0 car / RM 20,000 cash

Jay got 0 car / RM 15,000 cash

_______________________________

total...1 car / RM 35,000 cash

Later

Abu got 0 car / RM 20,000 cash

I.. got 1 car / RM 0 cash

Jay got 0 car / RM 15,000 cash

________________________________

total...1 car / RM 35,000 cash

Now

Abu got 0 car / RM 20,000 cash

I.. got 0 car / RM 15,000 cash

Jay got 1 car / RM 0 cash

________________________________

total...1 car / RM 35,000 cash

The car and the cash are just shifting between the 3 of us.

The total cash remain the same at RM 35,000.

I have less RM 5,000 but could we said Abu had earned RM 5,000 from me ?

There is no FINAL answer until we truly figure out the true value of the car.

What if Jay found RM 100,000 cash inside the car drawer ? Obviously, both,Abu and I just missed or actually LOSS the RM 100,000 to Jay !

What if the car totally "unrepairable" broke down forever, just 1 day after Jay bought it ? Wow ! Now I just earn RM 15,000 evernthough i have less RM 5,000 from my initial RM 20,000 bank balance ?

The moral will come back the same. Transacted price tell us not much. Sooner or later, it is the "true" value of the car that determined who make or who lose what.

.

Getting more Confused ?

.

Wisdom of Continuing the Business should be Considered

.

The question, viz., that of retaining the stockholders's capital in the business, involves considerations that are basically identical. Managements are naturally loath to return any part of the capital to its owners, eventhough this capital may be far more useful - and therefore valuable - outside of the business than in it. Returning a portion of the capital (eg., excess cash holdings) means curtailing the resources of the enterprise, perhaps creating financial problems later on and certainly reducing somewhat the prestige of the officers.

Complete liquidation means the loss of the job itself. It is scarcely to be expected, therefore, that the paid officers will considered the questions of continuing or winding up the business from the standpoint solely of what is the best interests of the owners. We must emphasize again that the directors are often so closely allied with the officers - who are themselves members of the board - that they too cannot be counted upon to consider such problems purely from the stockholders' point of view.

Thus it appears that the question whether or not a business should be continued is one that at times may deserve indepedent thought by its proprietors ~ the stockholders.

(It should be pointed out also that this is, by its formal or legal nature, an ownership problem and not a managemet problem.)

.

The question, viz., that of retaining the stockholders's capital in the business, involves considerations that are basically identical. Managements are naturally loath to return any part of the capital to its owners, eventhough this capital may be far more useful - and therefore valuable - outside of the business than in it. Returning a portion of the capital (eg., excess cash holdings) means curtailing the resources of the enterprise, perhaps creating financial problems later on and certainly reducing somewhat the prestige of the officers.

Complete liquidation means the loss of the job itself. It is scarcely to be expected, therefore, that the paid officers will considered the questions of continuing or winding up the business from the standpoint solely of what is the best interests of the owners. We must emphasize again that the directors are often so closely allied with the officers - who are themselves members of the board - that they too cannot be counted upon to consider such problems purely from the stockholders' point of view.

Thus it appears that the question whether or not a business should be continued is one that at times may deserve indepedent thought by its proprietors ~ the stockholders.

(It should be pointed out also that this is, by its formal or legal nature, an ownership problem and not a managemet problem.)

.

Saturday, December 11, 2010

Implications of Liquidating Value

.

Wall Street holds that liquidating value is of slight importance because the typical company has no intention of liquidating.

This view is logical, as far as it goes. When applied to a stock selling below break-up value, the Wall Street view may be amplified into the following :

"Although this stock would liquidate for more than its market price, it is not worth buying because :

1. the company cannot earn a satisfactory profit, and

2. it is not going to liquidate.

In the previous post suggested that the first assumption is likely to be wrong in a number of instances, for, although past earnings may have been disappointing, there is always a chance that through external or internal changes the concern may again earn a reasonable amount on its capital.

But in a considerable proportion of cases the pessimism of the market will at least appear to be justified.

We are led, therefore, to ask the question :

"Why is it that no matter how poor a corporation's prospect may seem, its owners permit it to remain in business until its resources are exhausted? "

.

Wall Street holds that liquidating value is of slight importance because the typical company has no intention of liquidating.

This view is logical, as far as it goes. When applied to a stock selling below break-up value, the Wall Street view may be amplified into the following :

"Although this stock would liquidate for more than its market price, it is not worth buying because :

1. the company cannot earn a satisfactory profit, and

2. it is not going to liquidate.

In the previous post suggested that the first assumption is likely to be wrong in a number of instances, for, although past earnings may have been disappointing, there is always a chance that through external or internal changes the concern may again earn a reasonable amount on its capital.

But in a considerable proportion of cases the pessimism of the market will at least appear to be justified.

We are led, therefore, to ask the question :

"Why is it that no matter how poor a corporation's prospect may seem, its owners permit it to remain in business until its resources are exhausted? "

.

Discrimination Required in Selecting "Stocks selling below Liquidating Value"

.

There is scarcely any doubt that common stocks selling well below liquidating value represent on the whole a class of undervalued securities. They have declined in price more severely than the actual conditions justify. This must mean that on the whole these stocks afford profitable opportunities for purchase.

Nevertheless, the securities analyst should exercise as much discrimination as possible in the choice of issues falling within this category. He will lean toward those for which he sees a fairly imminent prospect of some one of the favorable developments listed in "previous post."

Or else he will be partial to such as reveal other attractive statistical features besides their liquid-asset position, eg., satisfactory current earnings and dividends or a high average earning power in the past.

The analyst will avoid issues that have been losing their current assets at a rapid rate and show no definite signs of ceasing to do so.

There is scarcely any doubt that common stocks selling well below liquidating value represent on the whole a class of undervalued securities. They have declined in price more severely than the actual conditions justify. This must mean that on the whole these stocks afford profitable opportunities for purchase.

Nevertheless, the securities analyst should exercise as much discrimination as possible in the choice of issues falling within this category. He will lean toward those for which he sees a fairly imminent prospect of some one of the favorable developments listed in "previous post."

Or else he will be partial to such as reveal other attractive statistical features besides their liquid-asset position, eg., satisfactory current earnings and dividends or a high average earning power in the past.

The analyst will avoid issues that have been losing their current assets at a rapid rate and show no definite signs of ceasing to do so.

Apply Clear, Accurate Thinking

.

Examples of "UN-Clear" thinking are :

.

1. Blaming others or circumstances for our shortcomings.

2. Waiting for others to lead us instead of leading ourselves.

3. Wishing things were easier, instead of making ourselves better.

4. Wanting fewer chanllenges instead of developing more skills to handle them.

5. Wanting to be a millionaire without first becoming a thousandaire.

6. Saying things cost too much, instead of admitting we can't afford them.

.

.

CLEAR, Accurate thinking is vital to success.

Here are some tips :

.

1. Learn to separate facts from information.

2. Deal only with relevant facts.

3. Don't exaggerate or over-react.

4. Look for evidence before drawing conclusions.

5. Question everything, including your own assumptions.

6. Concentrate your effort and thought.

.

Examples of "UN-Clear" thinking are :

.

1. Blaming others or circumstances for our shortcomings.

2. Waiting for others to lead us instead of leading ourselves.

3. Wishing things were easier, instead of making ourselves better.

4. Wanting fewer chanllenges instead of developing more skills to handle them.

5. Wanting to be a millionaire without first becoming a thousandaire.

6. Saying things cost too much, instead of admitting we can't afford them.

.

.

CLEAR, Accurate thinking is vital to success.

Here are some tips :

.

1. Learn to separate facts from information.

2. Deal only with relevant facts.

3. Don't exaggerate or over-react.

4. Look for evidence before drawing conclusions.

5. Question everything, including your own assumptions.

6. Concentrate your effort and thought.

.

Sarawak Energy to finish six more projects by 2020

Saturday December 11, 2010

SIBU: Sarawak Energy Bhd (SEB) is focused on delivering six other hydro electricity dam projects besides the RM7.4bil Bakun and the RM3bil Murum dams before 2020. Chief executive officer Torstein Dale Sjotveit said these additions would represent 6,000- to 7,000-megawatt new capacity, which in turn would produce around 35,000 to 40,000 gigawatt hours of energy units. This is eight to nine times what we produce today, he said, adding that by 2020, SEB would be the leading producer of renewable energy in South-East Asia.

SESCO is a subsidiary of SEB.

Sjotveit said this clean renewable energy will power the development of the growing local markets, the establishment of new major industries and export to neighbouring countries like Brunei and Indonesia.

On the Bakun dam, he said SEB was committed to ensuring that energy from the dam, which is to be operational by next year, would be used to drive the state's economic growth. He also said SEB, on behalf of the state government, was now in the midst of a challenging negotiation with the federal government for Bakun's successful takeover.

On the Murum dam, he said its diversion tunnel was completed while the construction of the main dam was underway. On other projects, he said SEB had progressed negotiations with around 20 potential energy customers in Sarawak Corridor of Renewable Energy.

We are achieving price offering from them at 25% to 40% above what they offered last year. By this month too, we will be able to firm up agreements with at least four new customers in addition to the MEMC branch in Kuching and the Mukah Press Metal (second phase), he said.

Sjotveit is confident of a very strong financial performance for SEB this year. - Bernama

.

SIBU: Sarawak Energy Bhd (SEB) is focused on delivering six other hydro electricity dam projects besides the RM7.4bil Bakun and the RM3bil Murum dams before 2020. Chief executive officer Torstein Dale Sjotveit said these additions would represent 6,000- to 7,000-megawatt new capacity, which in turn would produce around 35,000 to 40,000 gigawatt hours of energy units. This is eight to nine times what we produce today, he said, adding that by 2020, SEB would be the leading producer of renewable energy in South-East Asia.

SESCO is a subsidiary of SEB.

Sjotveit said this clean renewable energy will power the development of the growing local markets, the establishment of new major industries and export to neighbouring countries like Brunei and Indonesia.

On the Bakun dam, he said SEB was committed to ensuring that energy from the dam, which is to be operational by next year, would be used to drive the state's economic growth. He also said SEB, on behalf of the state government, was now in the midst of a challenging negotiation with the federal government for Bakun's successful takeover.

On the Murum dam, he said its diversion tunnel was completed while the construction of the main dam was underway. On other projects, he said SEB had progressed negotiations with around 20 potential energy customers in Sarawak Corridor of Renewable Energy.

We are achieving price offering from them at 25% to 40% above what they offered last year. By this month too, we will be able to firm up agreements with at least four new customers in addition to the MEMC branch in Kuching and the Mukah Press Metal (second phase), he said.

Sjotveit is confident of a very strong financial performance for SEB this year. - Bernama

.

Friday, December 10, 2010

Psychology

.

The problem with trying to understand people, though, is that people are complex, and change all the time. We learn from our experiences, we form good intentions, and we are acted on by circumstances. So what we do can be influenced by a great many different factors. Also, everyone has their own ideas and opinions about what people are really like. These ideas can influenced what we do and also how we interpret what other people are doing. And since we each have had different lives, and have learned from our experiences, these ideas can be very different from one person to the next.

.

Collected 123,600 LCTH shares at 27.74 sen avg.

.

22.11.10 Buy LCTH 62,000 @ 0.2875

30.11.10 Buy LCTH 50,000 @ 0.2700

08.12.10 Buy LCTH 11,600 @ 0.2550

_____________________________

Total 123,600 LCTH shares @ 0.2774

_____________________________

Wish me LUCK !

Thanks.

.

22.11.10 Buy LCTH 62,000 @ 0.2875

30.11.10 Buy LCTH 50,000 @ 0.2700

08.12.10 Buy LCTH 11,600 @ 0.2550

_____________________________

Total 123,600 LCTH shares @ 0.2774

_____________________________

Wish me LUCK !

Thanks.

.

Perodua eyes bigger slice of car market in Nepal

Friday December 10, 2010

KATHMANDU: Perusahaan Otomobil Kedua Sdn Bhd (Perodua) aims to grab a bigger slice of the motor vehicle market in Nepal, despite the congested market which is largely dominated by Indian and Japanese makers.

Mihika Dhakhwa, managing director of Nemlink International Traders Pvt Ltd, the sole distributor of Perodua vehicles in Nepal, said regardless of the slow-paced economy and sluggish motor vehicle sector growth, demand was steadily rising.

“Next year will be better compared with 2010.

“We sold about 300 units of all Perodua models last year and hope to sell 400 units next year,” she told Bernama yesterday.

Mihika said the market was competitive and it was not easy to sell a third (brand) car.

“People did not have confidence in Malaysian cars earlier. But after nearly five years, we saw a major breakthrough. We rolled out about 100 units in 2006,” she said.

Though Nepal is grappling under a shaky government and a weak economy, it’s largely surviving on inflow of billion-dollar remittances from its nationals working overseas.

Its economy is growing at about 4.5% annually.

Ironically, car sales had shot up tremendously in recent years.

According to the Nepal Automobile Dealers Association, only 6,850 units (in the car/jeep/van category) were sold last year, but figures had easily doubled in 2010, touching nearly 12,268 units.

Mihika said overall, the car sector was growing in Nepal and more cars were on the road these days. “Now people are also confident of Malaysian cars.

“The customers are satisfied because of our after-sales service and Perodua’s maintenance cost is about 40% cheaper than the others,” she said.

Perodua models, such as Viva and MyVi, are gaining popularity in the Himalayan state, as these slick and economical vehicles best suit city driving. — Bernama

KATHMANDU: Perusahaan Otomobil Kedua Sdn Bhd (Perodua) aims to grab a bigger slice of the motor vehicle market in Nepal, despite the congested market which is largely dominated by Indian and Japanese makers.

Mihika Dhakhwa, managing director of Nemlink International Traders Pvt Ltd, the sole distributor of Perodua vehicles in Nepal, said regardless of the slow-paced economy and sluggish motor vehicle sector growth, demand was steadily rising.

“Next year will be better compared with 2010.

“We sold about 300 units of all Perodua models last year and hope to sell 400 units next year,” she told Bernama yesterday.

Mihika said the market was competitive and it was not easy to sell a third (brand) car.

“People did not have confidence in Malaysian cars earlier. But after nearly five years, we saw a major breakthrough. We rolled out about 100 units in 2006,” she said.

Though Nepal is grappling under a shaky government and a weak economy, it’s largely surviving on inflow of billion-dollar remittances from its nationals working overseas.

Its economy is growing at about 4.5% annually.

Ironically, car sales had shot up tremendously in recent years.

According to the Nepal Automobile Dealers Association, only 6,850 units (in the car/jeep/van category) were sold last year, but figures had easily doubled in 2010, touching nearly 12,268 units.

Mihika said overall, the car sector was growing in Nepal and more cars were on the road these days. “Now people are also confident of Malaysian cars.

“The customers are satisfied because of our after-sales service and Perodua’s maintenance cost is about 40% cheaper than the others,” she said.

Perodua models, such as Viva and MyVi, are gaining popularity in the Himalayan state, as these slick and economical vehicles best suit city driving. — Bernama

Thursday, December 9, 2010

Attractiveness of Stocks selling below Liquidating Value

.

Common stocks in this category practically always have an unsatisfactory trend of earnings. If the profits had been increasing steadily, it is obvious that the shares would not sell at so low a price.

.

The objection to buying these issues lies in the probability, or at least the possibility, that earnings will decline or losses continue and that the resources will be dissipated and the intrinsic value ultimately become less than the price paid. It may not be denied that this does actually happen in individual cases.

.

On the other hand, there is a much wider range of potential developments which may result in establishing a higher market price. These include the following:

.

1. The creation of an earning power commensurate with the company's assets. This may result from :

a) General improvement in the industry.

b) Favorable change in the company's operating policies, with or without a change in management. These changes include more efficient methods, new products, abandonment of umprofitable lines, etc.

.

2. A sale or merger, because some other concern is able to utilize the resources to better advantage and hence can pay at least liquidating value for assets.

.

3. Complete or partial liquidation.

.

Wednesday, December 8, 2010

Perodua to ramp up exports

KUALA LUMPUR: Perusahaan Otomobil Kedua Sdn Bhd (Perodua) aims to increase its exports to at least 10% or 20,000 units in line with its five-year roadmap besides developing further the vendor community so that they too boost their exports of auto parts.

Although we are relatively strong in the domestic market, at some point in time, the domestic car market will not grow as much, nearing saturation. By that time, we need to be globally competitive to survive, and this is why we need to seriously look into exports, managing director Datuk Aminar Rashid Salleh said in an interview recently. Currently, the national carmaker is exporting only 2% to 3% of its total output.

Things were not as rosy as they seemed for the local car market, Aminar said, adding that it could be approaching its saturation point based on demand and the population. This year alone, MAA (Malaysian Automotive Association) forecast the total industry volume (TIV) to hit 570,000 units, which will be the highest ever in the automotive history of the country, he said.

Comparing Malaysia with Taiwan based on the similarities in population, he said Taiwan reached its saturation point somewhere at a TIV of 800,000 units. We will be reaching the 600,000th mark next year and in the next five to seven years, the local car market may hit a saturation point, dampening any growth potential.

This is the reason we want to contribute and develop the local vendor community so that they can become globally paced as well, he said. Currently, the carmaker is supported by 141 vendors, with local vendors comprising 60%-70% while the rest are joint-venture companies with foreign partners or independent foreign companies.

This is something we are doing to give back to the community; by generating the socio-economic development needed, creating jobs, and purchasing local parts. We purchase these locally made parts to the tune of RM3bil to RM4bil a year, said Aminar.

However, he said vendors faced a high turnover of workers. There must be more concerted effort from the industry, manufacturers and the Government to tackle this problem; to reduce the dependency on foreign workers and increase the participation of locals. The quality of components will obviously be affected as new workers need to be retrained, he said.

These vendors had helped with the localisation of the cars, he said, citing the Perodua Alza which had 90% local content. Aminar said 75% of Perodua's sales and services were undertaken by independent entrepreneurs. We are creating business opportunities for our dealers and providing them not only with products, but also training development to make sure they are competent, he said.

To date, Perodua has invested about RM3bil mainly for its plant as well as its sales and distribution division, to the extent that there are more independent dealers than its own outlets. It currently has more than 11,000 employees, of whom 8,000 work at its plant in Rawang.

Aminar said Perodua also aimed to at least double its engine components export business to RM50mil by increasing trade around the South-East Asia region in the next three years. We are at the tail-end of a feasibility study to export to Thailand and we are currently exporting to countries like Pakistan, Indonesia and Japan, he said. The company is also looking at opportunities to export completely-built-up units to South Africa.

Perodua's shareholders are UMW Corp Sdn Bhd, which holds a 38% equity; Daihatsu Motor Co Ltd of Japan, 20%; MBM Resources Sdn Bhd also 20%; PNB Equity Resources Corp Sdn Bhd 10%; Mitsui & Co Ltd 7% and Daihatsu (M) Sdn Bhd 5%.

On Perodua's foreign partner, Aminar said the relationship with Daihatsu had been a successful partnership. The important factor with Daihatsu is that they have been around much longer and are more knowledgeable with vast experience, not just in technical aspects but also technology that involves huge sums of money. It helps small players like us understand the challenges to being export-driven, sharing of resources and platform, as well as huge amount of data that we can benchmark ourselves against, he said.

On car sales, he said as at end-October, Perodua was the top selling carmaker with a market share of 31.1% at 157,200 units. Our target to sell 185,000 cars this year is achievable and we have already revised upwards next year's target to 190,000 units. He attributed the stellar performance to star model, the Myvi, which contributed 41.1% to total sales this year, followed by the Viva, which accounted for 37%, and Alza 22%.

Competition is everywhere and it has kept us on our toes all the time. Customers have a choice and our performance is determined by them, he said. We are driven by market forces. We had put a lot of emphasis on the whole gambit of the auto business like our showrooms, networks, customer cars, product line-up improvement and retention programme.

Aminar said he hoped Perodua would retain its top spot on the country's car sellers list this year for the fifth consecutive year. - Bernama

Although we are relatively strong in the domestic market, at some point in time, the domestic car market will not grow as much, nearing saturation. By that time, we need to be globally competitive to survive, and this is why we need to seriously look into exports, managing director Datuk Aminar Rashid Salleh said in an interview recently. Currently, the national carmaker is exporting only 2% to 3% of its total output.

Things were not as rosy as they seemed for the local car market, Aminar said, adding that it could be approaching its saturation point based on demand and the population. This year alone, MAA (Malaysian Automotive Association) forecast the total industry volume (TIV) to hit 570,000 units, which will be the highest ever in the automotive history of the country, he said.

Comparing Malaysia with Taiwan based on the similarities in population, he said Taiwan reached its saturation point somewhere at a TIV of 800,000 units. We will be reaching the 600,000th mark next year and in the next five to seven years, the local car market may hit a saturation point, dampening any growth potential.

This is the reason we want to contribute and develop the local vendor community so that they can become globally paced as well, he said. Currently, the carmaker is supported by 141 vendors, with local vendors comprising 60%-70% while the rest are joint-venture companies with foreign partners or independent foreign companies.

This is something we are doing to give back to the community; by generating the socio-economic development needed, creating jobs, and purchasing local parts. We purchase these locally made parts to the tune of RM3bil to RM4bil a year, said Aminar.

However, he said vendors faced a high turnover of workers. There must be more concerted effort from the industry, manufacturers and the Government to tackle this problem; to reduce the dependency on foreign workers and increase the participation of locals. The quality of components will obviously be affected as new workers need to be retrained, he said.

These vendors had helped with the localisation of the cars, he said, citing the Perodua Alza which had 90% local content. Aminar said 75% of Perodua's sales and services were undertaken by independent entrepreneurs. We are creating business opportunities for our dealers and providing them not only with products, but also training development to make sure they are competent, he said.

To date, Perodua has invested about RM3bil mainly for its plant as well as its sales and distribution division, to the extent that there are more independent dealers than its own outlets. It currently has more than 11,000 employees, of whom 8,000 work at its plant in Rawang.

Aminar said Perodua also aimed to at least double its engine components export business to RM50mil by increasing trade around the South-East Asia region in the next three years. We are at the tail-end of a feasibility study to export to Thailand and we are currently exporting to countries like Pakistan, Indonesia and Japan, he said. The company is also looking at opportunities to export completely-built-up units to South Africa.

Perodua's shareholders are UMW Corp Sdn Bhd, which holds a 38% equity; Daihatsu Motor Co Ltd of Japan, 20%; MBM Resources Sdn Bhd also 20%; PNB Equity Resources Corp Sdn Bhd 10%; Mitsui & Co Ltd 7% and Daihatsu (M) Sdn Bhd 5%.

On Perodua's foreign partner, Aminar said the relationship with Daihatsu had been a successful partnership. The important factor with Daihatsu is that they have been around much longer and are more knowledgeable with vast experience, not just in technical aspects but also technology that involves huge sums of money. It helps small players like us understand the challenges to being export-driven, sharing of resources and platform, as well as huge amount of data that we can benchmark ourselves against, he said.

On car sales, he said as at end-October, Perodua was the top selling carmaker with a market share of 31.1% at 157,200 units. Our target to sell 185,000 cars this year is achievable and we have already revised upwards next year's target to 190,000 units. He attributed the stellar performance to star model, the Myvi, which contributed 41.1% to total sales this year, followed by the Viva, which accounted for 37%, and Alza 22%.

Competition is everywhere and it has kept us on our toes all the time. Customers have a choice and our performance is determined by them, he said. We are driven by market forces. We had put a lot of emphasis on the whole gambit of the auto business like our showrooms, networks, customer cars, product line-up improvement and retention programme.

Aminar said he hoped Perodua would retain its top spot on the country's car sellers list this year for the fifth consecutive year. - Bernama

Monday, December 6, 2010

Financial Reasoning vs Business Reasoning

We have here the point that brings home strikingly perhaps than any other the widened rift between financial thought and ordinary business thought. It is an almost unbelievable fact that Wall Street never asks, "How much is the business is selling for ?" Yet this should be the first question in considering a stock purchase.

.

If a business man were offered a 5% interest in some concern for $10,000, his first mental process would be to multiply the asked priceby 20 and thus establish a proposed value of $200,000 for the entire undertaking. The rest of his calculation would turn about the question whether or not the business was a "good buy" at $200,000.

.

This elementary and indispensable approach has been practically abandoned by those who purchase stocks.

.

Recomendation.

.

These examples, extreme as they are, suggest rather forcibly that the book value deserves at least a fleeting glance by the public before it buys or sells shares in a business undertaking. In any particular case the message that the book value conveys may well prove to be inconsequential and unworthy of attention.

.

But this testimony should be examined before it is rejected. Let the stock buyer, if he lay any claim to intelligence, at least be able to tell himself, first, what value he is actually setting on the business and, second, what he is actually getting for his money in terms of tangible resources.

.

Tuesday, November 30, 2010

Practical Significance of Book Value

.

The book value of a common stock was originally the most important element in its financial exhibit. It was supposed to show "the value" of the shares in the same way as a merchant's balance sheet shows him the value of his business. This idea has almost completely disappeared from the financial horizon. The value of a company's assets as carried in its balance sheet has lost practically all its significance.

.

This change arose from the fact,

~first, that the value of the fixed assets, as stated,

frequently bore no relationship to the actual cost and,

~secondly that in an even larger proportion of cases

these values bore no relationship to the figure at which they would be sold

or the figure which would be justified by the earnings.

.

The practice of inflating the book value of the fixed property is giving way to the opposite artifice of cutting it down to nothing in order to avoid depreciation charges, but both have the same consequence of depriving the book-value figures of any real significance.

.

It is a bit strange, like quaint survival from the past, that the leading statistical services still maintain the old procedure of calculating the book value per share of common stock from many, perhaps most, balance sheets that they publish.

.

Before we discard completely this time-honored conception of book value, let us ask if it may ever have practical significance for the analyst. In the ordinary case, probably not. But what of the extraordinary or extreme case ?

.

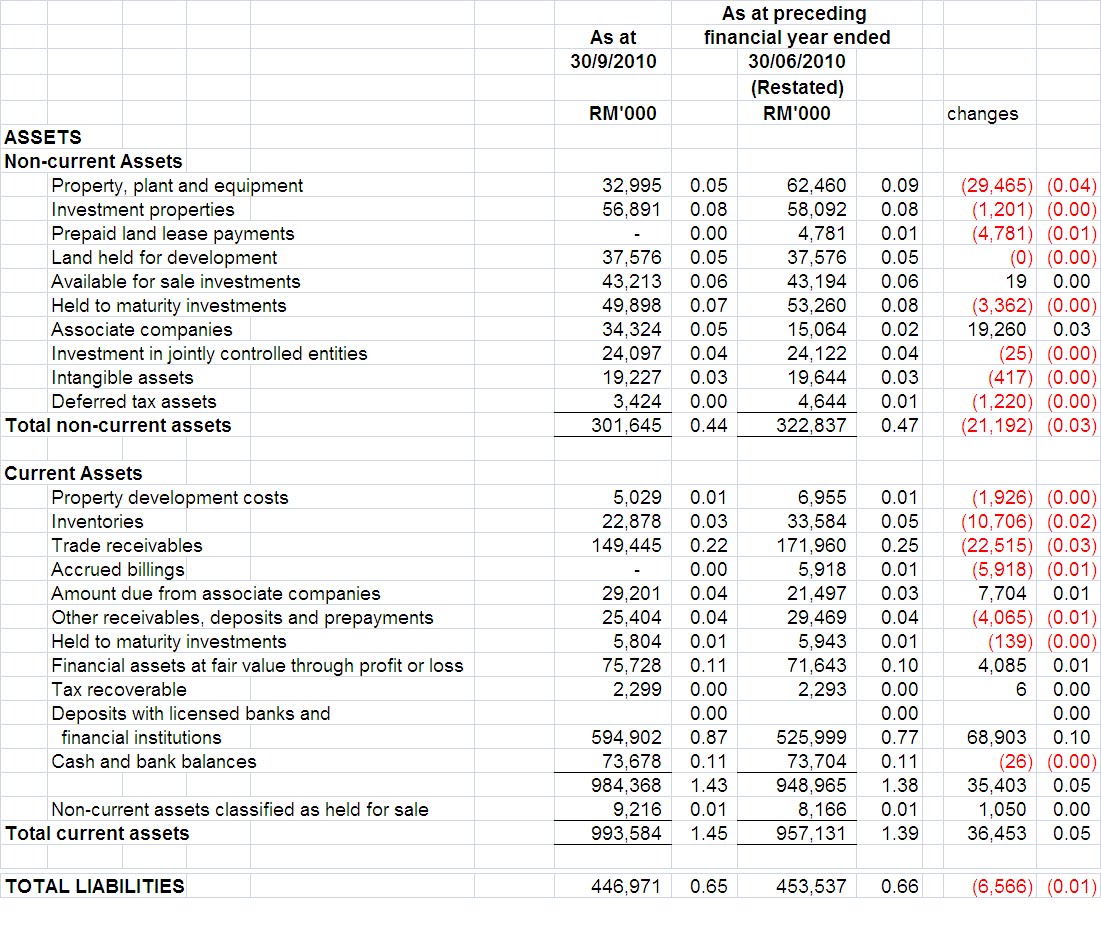

Insas ~ 2011 Q3 report

01 Dec 2010 ~ current price 52.5 sen

Insas cash RM 595 million (87 sen per share)

Total Liabilities RM 447 million (65 sen per share)

Therefore just "net Cash" alone stand at = 595-447 = RM 148 million (22 sen per share)

Very STRONG balance sheet.

.

Next, is to identified the "Cash equavalent" elements and group them together.

Berkshire Chairman's Letter ~ 1978

.

We confess considerable optimism regarding our insurance

equity investments. Of course, our enthusiasm for stocks is not

unconditional. Under some circumstances, common stock

investments by insurers make very little sense.

We get excited enough to commit a big percentage of

insurance company net worth to equities only when we find

(1) businesses we can understand,

(2) with favorable long-term prospects,

(3) operated by honest and competent people, and

(4) priced very attractively.

We usually can identify a small number

of potential investments meeting requirements (1), (2) and (3),

but (4) often prevents action.

For example, in 1971 our total common stock position

at Berkshire’s insurance subsidiaries amounted to only $10.7 million at cost,

and $11.7 million at market.

There were equities of identifiably excellent companies

available - but very few at interesting prices.

(An irresistible footnote: in 1971, pension fund managers invested a record 122%

of net funds available in equities - at full prices they couldn’t buy enough of them.

In 1974, after the bottom had fallen out,

they committed a then record low of 21% to stocks.)

The past few years have been a different story for us.

At the end of 1975 our insurance subsidiaries held common equities

with a market value exactly equal to cost of $39.3 million.

At the end of 1978 this position had been increased to equities

(including a convertible preferred) with a cost of $129.1 million

and a market value of $216.5 million.

During the intervening three years we also had realized pre-tax gains

from common equities of approximately $24.7 million.

Therefore, our overall unrealized and realized pre-tax gains in equities

for the three year period came to approximately $112 million.

During this same interval the Dow-Jones Industrial Average

declined from 852 to 805.

It was a marvelous period for the value-oriented equity buyer.

We continue to find for our insurance portfolios small

portions of really outstanding businesses that are available,

through the auction pricing mechanism of security markets,

at prices dramatically cheaper than the valuations inferior

businesses command on negotiated sales.

This program of acquisition of small fractions of businesses

(common stocks) at bargain prices, for which little enthusiasm exists,

contrasts sharply with general corporate acquisition activity,

for which much enthusiasm exists.

It seems quite clear to us that either corporations are making

very significant mistakes in purchasing entire businesses at prices

prevailing in negotiated transactions and takeover bids,

or that we eventually are going to make considerable sums of money buying

small portions of such businesses at the greatly discounted valuations

prevailing in the stock market.

(A second footnote: in 1978 pension managers,

a group that logically should maintain the longest of investment perspectives,

put only 9% of net available funds into equities

- breaking the record low figure set in 1974 and tied in 1977.)

We are not concerned with whether the market quickly

revalues upward securities that we believe are selling at bargain

prices. In fact, we prefer just the opposite since, in most

years, we expect to have funds available to be a net buyer of

securities. And consistent attractive purchasing is likely to

prove to be of more eventual benefit to us than any selling

opportunities provided by a short-term run up in stock prices to

levels at which we are unwilling to continue buying.

Our policy is to concentrate holdings. We try to avoid

buying a little of this or that when we are only lukewarm about

the business or its price. When we are convinced as to

attractiveness, we believe in buying worthwhile amounts.

.

We confess considerable optimism regarding our insurance

equity investments. Of course, our enthusiasm for stocks is not

unconditional. Under some circumstances, common stock

investments by insurers make very little sense.

We get excited enough to commit a big percentage of

insurance company net worth to equities only when we find

(1) businesses we can understand,

(2) with favorable long-term prospects,

(3) operated by honest and competent people, and

(4) priced very attractively.

We usually can identify a small number

of potential investments meeting requirements (1), (2) and (3),

but (4) often prevents action.

For example, in 1971 our total common stock position

at Berkshire’s insurance subsidiaries amounted to only $10.7 million at cost,

and $11.7 million at market.

There were equities of identifiably excellent companies

available - but very few at interesting prices.

(An irresistible footnote: in 1971, pension fund managers invested a record 122%

of net funds available in equities - at full prices they couldn’t buy enough of them.

In 1974, after the bottom had fallen out,

they committed a then record low of 21% to stocks.)

The past few years have been a different story for us.

At the end of 1975 our insurance subsidiaries held common equities

with a market value exactly equal to cost of $39.3 million.

At the end of 1978 this position had been increased to equities

(including a convertible preferred) with a cost of $129.1 million

and a market value of $216.5 million.

During the intervening three years we also had realized pre-tax gains

from common equities of approximately $24.7 million.

Therefore, our overall unrealized and realized pre-tax gains in equities

for the three year period came to approximately $112 million.

During this same interval the Dow-Jones Industrial Average

declined from 852 to 805.

It was a marvelous period for the value-oriented equity buyer.

We continue to find for our insurance portfolios small

portions of really outstanding businesses that are available,

through the auction pricing mechanism of security markets,

at prices dramatically cheaper than the valuations inferior

businesses command on negotiated sales.

This program of acquisition of small fractions of businesses

(common stocks) at bargain prices, for which little enthusiasm exists,

contrasts sharply with general corporate acquisition activity,

for which much enthusiasm exists.

It seems quite clear to us that either corporations are making

very significant mistakes in purchasing entire businesses at prices

prevailing in negotiated transactions and takeover bids,

or that we eventually are going to make considerable sums of money buying

small portions of such businesses at the greatly discounted valuations

prevailing in the stock market.

(A second footnote: in 1978 pension managers,

a group that logically should maintain the longest of investment perspectives,

put only 9% of net available funds into equities

- breaking the record low figure set in 1974 and tied in 1977.)

We are not concerned with whether the market quickly

revalues upward securities that we believe are selling at bargain

prices. In fact, we prefer just the opposite since, in most

years, we expect to have funds available to be a net buyer of

securities. And consistent attractive purchasing is likely to

prove to be of more eventual benefit to us than any selling

opportunities provided by a short-term run up in stock prices to

levels at which we are unwilling to continue buying.

Our policy is to concentrate holdings. We try to avoid

buying a little of this or that when we are only lukewarm about

the business or its price. When we are convinced as to

attractiveness, we believe in buying worthwhile amounts.

.

Insas ~ Annual Report 2010

For financial year end 30 june 2010, the Group achieved profits of 54 million compared to RM 57 million for the precious year.

.

The business environment was volatile last year, dominated by China and other international events, The financial year began quite favorably in July last year as financial markets appeared to be recovering well from the financial crash of October 2008 when Lehman Brothers (a major Wall Street firm) collapsed. However, at the end of November 2009, Dubai World defaulted on its loans to a consortioum of international banks. In December, the Greek Sovereign debt crisis became contagion and triggered a crisis of confidence in the stability of the European Union, and caused the Euro to drop sharply by about 21% in 5 months. This affected global investors' confidence badly, and financial and stock markets declined. Despite the recent recovery in stock markets, the US goverment just announced another round of "quantitative easing" to prevent a double dip recession.

.

In terms of operations, our investment management, project finance and IT divisions were the main earners, contributing profits of RM 24 million, RM 16 million and RM 14 million respectively.

.

Our stock brocking division's performance was satisfactory in light of low trading volumes on Bursa. We are trying to increase our presence and market share by opening branches in other states as a long term strategy. However, I am pleased to report that our corporate finace division was profitable in its first year of operations as it managed to to secure several advisory mandates for capital raising and initial public offerings.

.

Our high fashion retail business under Melium has rebounded quite strongly and we expect next year's performance to return to almost pre-crisis level. With the recent announcement of abolition of taxes on luxury goods, Malaysis will become as competitive as Singapore and Hong Kong for luxury goods. The goverment has also allocated increased budget to the Ministry of Tourism in a serious effort to increase the number of visitors to Malaysia. We expect all these positive factors to be favourable for our business.

.

Last year, we reported that we made a sizeable investment in London in Chantrey House, a residential cum commercial property in the Belgravia area, a prime property location with our UK partner, we took an equal interest in the investment amounting to 22.5 million British Pounds. Since we purchased that property, central London property prices have recovered strongly. Current prices for apartments in comparable locations are transacting at between 1,200 to 1,400 Pounds per square feet compared to our purchase price of 670 Pounds per square feet. We intend to hold on to this investment as we believe property prices should continue to rise in view of the low interest rate environment.

.

We ended the financial year with a strong and liquid balance sheet. We are continueing to look for new investments that can provide the Group with sustainable earnings in the future.

.

.

Dato' Thong Kok Khee

Executive Deputy Chairman/

Chief Executive Officer.

.

Sunday, November 28, 2010

SPNB awards RM1.7bil jobs for LRT extension

Saturday November 27, 2010

PETALING JAYA: Syarikat Prasarana Negara Bhd (SPNB) has awarded contracts worth RM1.7bil for the first phase (Package A) of the RM7bil light rail transit (LRT) extension project involving the Kelana Jaya and Ampang lines.

In a statement yesterday, SPNB, which was established by the Finance Ministry to facilitate, undertake and expedite infrastructure projects for the Government, said the main contractor facilities job for Package A of the Kelana Jaya line, valued at RM950mil, was awarded to Trans Resources Corp Bhd. The work will take 30 months to complete.

UEM Builders Bhd and Intria Bina Sdn Bhd were jointly appointed the nominated sub-contractors for the fabrication and delivery of segmental box girder jobs worth RM93.16mil, which is expected to take 21 months to complete.

Package A of the Kelana Jaya line will be a 9.2km extension from the Kelana Jaya station to Summit (Station 7). Package B will involve a 7.8km extension from Station 7 to the Putra Heights station.

Meanwhile, the main contractor facilities job for Package A of the Ampang line was jointly awarded to Bina Puri Holdings Bhd and Tim Sekata. Valued at RM634.64mil, the work will take 27 months to complete.

Bina Puri and Tim Sekata were also jointly appointed the nominated sub-contractors for the fabrication and delivery of segmental box girder jobs, which is valued at RM67.70mil and expected to take 19 months to complete.

Package A of the Ampang line will be a new 7.4km stretch from the Seri Petaling station to Station No. 5, while Package B will see a 10.3km extension from Station No. 5 to the Putra Heights Station.

SPNB said recipients of the main contractor facilities jobs would be responsible for all guideway sub-structure and main structure works, foundation work for stations and traction power sub-stations (TPSS), to launch and install segmental box girders and to supply and install parapets and noise barriers.

In addition, within the total contract value, the main contractors will also manage the nominated sub-contractors for contracts worth RM469mil (Kelana Jaya line) and RM305mil (Ampang line).

SPNB said the selection of the contractors was done through an open-tender process starting from November 2009. A total of 119 applications were received, but one was rejected due to failure to comply with application guidelines.

The tender for the facilities works under Package B for both lines will be called upon approval of the final railway scheme, which is expected by mid-2011.

With the appointment of the main contractors, it is expected that work on the line extension projects will start as soon as possible, SPNB said.

PETALING JAYA: Syarikat Prasarana Negara Bhd (SPNB) has awarded contracts worth RM1.7bil for the first phase (Package A) of the RM7bil light rail transit (LRT) extension project involving the Kelana Jaya and Ampang lines.

In a statement yesterday, SPNB, which was established by the Finance Ministry to facilitate, undertake and expedite infrastructure projects for the Government, said the main contractor facilities job for Package A of the Kelana Jaya line, valued at RM950mil, was awarded to Trans Resources Corp Bhd. The work will take 30 months to complete.

UEM Builders Bhd and Intria Bina Sdn Bhd were jointly appointed the nominated sub-contractors for the fabrication and delivery of segmental box girder jobs worth RM93.16mil, which is expected to take 21 months to complete.

Package A of the Kelana Jaya line will be a 9.2km extension from the Kelana Jaya station to Summit (Station 7). Package B will involve a 7.8km extension from Station 7 to the Putra Heights station.

Meanwhile, the main contractor facilities job for Package A of the Ampang line was jointly awarded to Bina Puri Holdings Bhd and Tim Sekata. Valued at RM634.64mil, the work will take 27 months to complete.

Bina Puri and Tim Sekata were also jointly appointed the nominated sub-contractors for the fabrication and delivery of segmental box girder jobs, which is valued at RM67.70mil and expected to take 19 months to complete.

Package A of the Ampang line will be a new 7.4km stretch from the Seri Petaling station to Station No. 5, while Package B will see a 10.3km extension from Station No. 5 to the Putra Heights Station.

SPNB said recipients of the main contractor facilities jobs would be responsible for all guideway sub-structure and main structure works, foundation work for stations and traction power sub-stations (TPSS), to launch and install segmental box girders and to supply and install parapets and noise barriers.

In addition, within the total contract value, the main contractors will also manage the nominated sub-contractors for contracts worth RM469mil (Kelana Jaya line) and RM305mil (Ampang line).

SPNB said the selection of the contractors was done through an open-tender process starting from November 2009. A total of 119 applications were received, but one was rejected due to failure to comply with application guidelines.

The tender for the facilities works under Package B for both lines will be called upon approval of the final railway scheme, which is expected by mid-2011.

With the appointment of the main contractors, it is expected that work on the line extension projects will start as soon as possible, SPNB said.

Intro Balance Sheet Analysis ~ Bruce Greenwald

The enduring value of Security Analysis rests on certain critical ideas that were then, and remain, fundamental to any well-conceived investment strategy. The first of these is the distintion between "investment" and "speculation" as defined by Graham and Dodd :

An investment operation is one which, upon thorough analysis,

promises safety of principal and a satisfactory return.

Operations not meeting these requirements are speculative.

The critical parts of this definition are "thorough analysis" and "safety of principal and a satisfactory return." Nothing about these requirements has changed since 1934.

A second related idea is that of focusing on the intrinsic of a security. It is according to Graham and Dodd,

that value which is justified by the facts,

eg., the assets, earnings, dividends, [and] definite prospects,

as distinct, let us say, from market quotations

established by market manipulation or distorted by psychological excesses.

.

An investment operation is one which, upon thorough analysis,

promises safety of principal and a satisfactory return.

Operations not meeting these requirements are speculative.

The critical parts of this definition are "thorough analysis" and "safety of principal and a satisfactory return." Nothing about these requirements has changed since 1934.

A second related idea is that of focusing on the intrinsic of a security. It is according to Graham and Dodd,

that value which is justified by the facts,

eg., the assets, earnings, dividends, [and] definite prospects,

as distinct, let us say, from market quotations

established by market manipulation or distorted by psychological excesses.

.

Saturday, November 27, 2010

Berkshire Chairman's Letter 1977

We select our marketable equity securities in much the same

way we would evaluate a business for acquisition in its entirety.

We want the business to be

(1) one that we can understand,

(2) with favorable long-term prospects,

(3) operated by honest and competent people, and

(4) available at a very attractive price.

We ordinarily make no attempt to buy equities for anticipated

favorable stock price behavior in the short term. In fact, if

their business experience continues to satisfy us, we welcome

lower market prices of stocks we own as an opportunity to acquire

even more of a good thing at a better price.

Our experience has been that pro-rata portions of truly

outstanding businesses sometimes sell in the securities markets

at very large discounts from the prices they would command in

negotiated transactions involving entire companies.

Consequently, bargains in business ownership, which simply are

not available directly through corporate acquisition, can be

obtained indirectly through stock ownership. When prices are

appropriate, we are willing to take very large positions in

selected companies, not with any intention of taking control and

not foreseeing sell-out or merger, but with the expectation that

excellent business results by corporations will translate over

the long term into correspondingly excellent market value and

dividend results for owners, minority as well as majority.

Such investments initially may have negligible impact on our

operating earnings. For example, we invested $10.9 million in

Capital Cities Communications during 1977. Earnings attributable

to the shares we purchased totaled about $1.3 million last year.

But only the cash dividend, which currently provides $40,000

annually, is reflected in our operating earnings figure.

Capital Cities possesses both extraordinary properties and

extraordinary management. And these management skills extend

equally to operations and employment of corporate capital. To

purchase, directly, properties such as Capital Cities owns would

cost in the area of twice our cost of purchase via the stock

market, and direct ownership would offer no important advantages

to us. While control would give us the opportunity - and the

responsibility - to manage operations and corporate resources, we

would not be able to provide management in either of those

respects equal to that now in place. In effect, we can obtain a

better management result through non-control than control. This

is an unorthodox view, but one we believe to be sound.

.

way we would evaluate a business for acquisition in its entirety.

We want the business to be

(1) one that we can understand,

(2) with favorable long-term prospects,

(3) operated by honest and competent people, and

(4) available at a very attractive price.

We ordinarily make no attempt to buy equities for anticipated

favorable stock price behavior in the short term. In fact, if

their business experience continues to satisfy us, we welcome

lower market prices of stocks we own as an opportunity to acquire

even more of a good thing at a better price.

Our experience has been that pro-rata portions of truly

outstanding businesses sometimes sell in the securities markets

at very large discounts from the prices they would command in

negotiated transactions involving entire companies.

Consequently, bargains in business ownership, which simply are

not available directly through corporate acquisition, can be

obtained indirectly through stock ownership. When prices are

appropriate, we are willing to take very large positions in

selected companies, not with any intention of taking control and

not foreseeing sell-out or merger, but with the expectation that

excellent business results by corporations will translate over

the long term into correspondingly excellent market value and

dividend results for owners, minority as well as majority.

Such investments initially may have negligible impact on our

operating earnings. For example, we invested $10.9 million in

Capital Cities Communications during 1977. Earnings attributable

to the shares we purchased totaled about $1.3 million last year.

But only the cash dividend, which currently provides $40,000

annually, is reflected in our operating earnings figure.

Capital Cities possesses both extraordinary properties and

extraordinary management. And these management skills extend

equally to operations and employment of corporate capital. To

purchase, directly, properties such as Capital Cities owns would

cost in the area of twice our cost of purchase via the stock

market, and direct ownership would offer no important advantages

to us. While control would give us the opportunity - and the

responsibility - to manage operations and corporate resources, we

would not be able to provide management in either of those